If you spend any time around rental property analysis, you will hear two metrics constantly: NOI and cap rate. They are tightly related, but they are not interchangeable. New investors often mix them up, which leads to sloppy property comparisons and poor pricing decisions.

The simplest way to think about it is this:

- NOI tells you the dollars the property produces before debt service

- Cap rate tells you how large that NOI is relative to the price

That difference matters. A property can have strong NOI in absolute dollars and still be overpriced. A property can also have a decent cap rate but weak total cash flow once financing and reserves are added back in.

Short version: NOI is the operating income. Cap rate is the yield on price. You need both.

NOI Definition

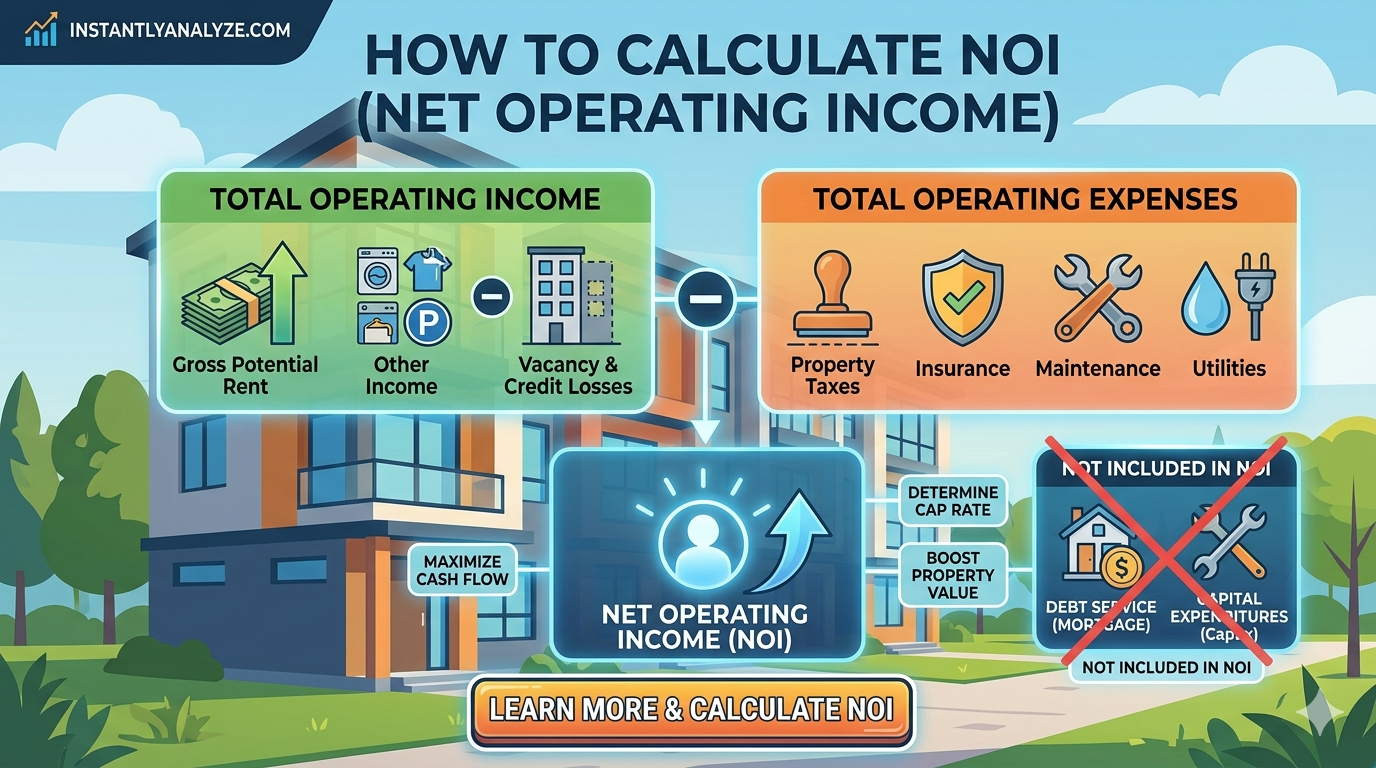

Net Operating Income (NOI) is the property's annual income after operating expenses but before mortgage payments, income taxes, depreciation, and capital structure.

Formula:

NOI = Gross Operating Income - Operating Expenses

For a rental property, that typically means:

- collected rent and other recurring income

- minus taxes

- minus insurance

- minus maintenance

- minus management

- minus vacancy allowance

- minus utilities paid by owner

- minus recurring operating costs

Cap Rate Definition

Cap rate converts NOI into a percentage based on the property's purchase price or market value.

Formula:

Cap Rate = NOI / Purchase Price

If a property produces $12,000 in annual NOI and costs $200,000, the cap rate is 6%.

Why Investors Use Both

Use NOI to understand the business

NOI helps you answer:

- How much income does this property really throw off before debt?

- Are expenses too high for the rent level?

- Is operational improvement likely to create value?

NOI is especially useful when you are deciding whether a property has value-add potential. If you can raise rent, reduce vacancy, or control expenses, NOI improves directly.

Use cap rate to compare pricing

Cap rate helps you answer:

- Am I paying too much for this income stream?

- How does this property compare with similar deals in the same market?

- What value does a given NOI support at my target yield?

Cap rate is the bridge between income and valuation. That is why brokers, appraisers, and experienced investors use it to frame price discussions.

Example: Same NOI, Different Pricing

Suppose two properties each produce $18,000 in annual NOI.

| Property | Price | NOI | Cap Rate |

|---|---|---|---|

| Property A | $300,000 | $18,000 | 6.0% |

| Property B | $360,000 | $18,000 | 5.0% |

The operations look the same from an NOI perspective. But the pricing is different. Property A is cheaper for the same income stream, so the cap rate is higher.

If your market standard is around 6%, Property B may be overpriced unless it has stronger appreciation upside, lower risk, or clear rent growth potential.

Free to use. No credit card needed. See cash flow, cap rate, and ROI in minutes.

Start Analyzing — FreeCommon Mistake: Using Cap Rate Without Understanding NOI Quality

A cap rate is only as good as the NOI behind it.

If the seller understates maintenance, ignores turnover, or uses unrealistic rent assumptions, the quoted cap rate becomes meaningless. That is why disciplined investors first pressure-test the NOI inputs and only then compare cap rates.

This is also where quick rules like the 50% rule help. They are not perfect, but they provide a fast sanity check before you trust a seller pro forma.

Common Mistake: Using NOI Alone to Judge a Deal

NOI by itself does not tell you whether the property is attractively priced.

A 20-unit building with $120,000 of NOI sounds impressive. But if the price is $2.8 million, the yield may be weaker than a smaller building with lower NOI and a better entry price.

That is why serious underwriting moves through a sequence:

- Estimate realistic income

- Estimate realistic expenses

- Calculate NOI

- Convert NOI to cap rate

- Layer in financing to get cash-on-cash return and cash flow

Which Metric Matters More?

For early deal screening:

- NOI matters more if you are diagnosing operations

- Cap rate matters more if you are comparing price

For final decision-making, neither is enough on its own. You still need debt service, cash needed, reserve assumptions, rehab costs, and exit risk.

Practical Investor Workflow

A clean workflow looks like this:

- Use gross rent and the 50% rule to screen quickly

- Build a real expense estimate and calculate NOI

- Convert NOI into cap rate to judge pricing

- Run the full property through a calculator to see cash flow, CoC ROI, and downside scenarios

The key is not picking a favorite metric. The key is understanding what question each metric answers.

Ready to compare NOI, cap rate, cash flow, and financing side by side? Run a full property analysis and let the numbers stack together in one report.

NOI explains operations. Cap rate explains price. Learn both, and you will make much better buy, pass, and negotiate decisions.