If you want to know how to invest in real estate with rental properties, most of the skill is in separating deals worth analyzing from ones you should skip. The 1% rule is the fastest tool for that job. It gives you a yes/no answer in about five seconds, which matters when you're evaluating 30 listings before deciding which three deserve a full look.

This guide covers why real estate is worth investing in, what the 1% rule is and how to apply it, how it compares to the stricter 2% rule, and what real estate investment tips and metrics actually matter once a property passes the initial screen.

Quick take: The 1% rule is a triage filter. Properties that fail can usually be eliminated fast. Properties that pass still need full underwriting before you commit.

Why the 1% rule matters for how to invest in real estate

Real estate is one of the few investments where you can use borrowed money to control a large asset, earn income while it appreciates, and reduce your tax bill at the same time.

Rental properties have four return drivers working at once: monthly cash flow from rent, appreciation as the property's value grows, principal paydown as your tenant effectively retires your mortgage, and tax advantages through depreciation and deductions. No other common asset class stacks all four. A stock pays dividends or appreciates; it does not let you borrow at 5–7% to control a $300,000 asset with $60,000 down.

Types of real estate investments

The most common entry point for individual investors is the single-family or small multifamily rental. Other options include:

- House hacking — living in one unit of a duplex or triplex while tenants cover most of your mortgage

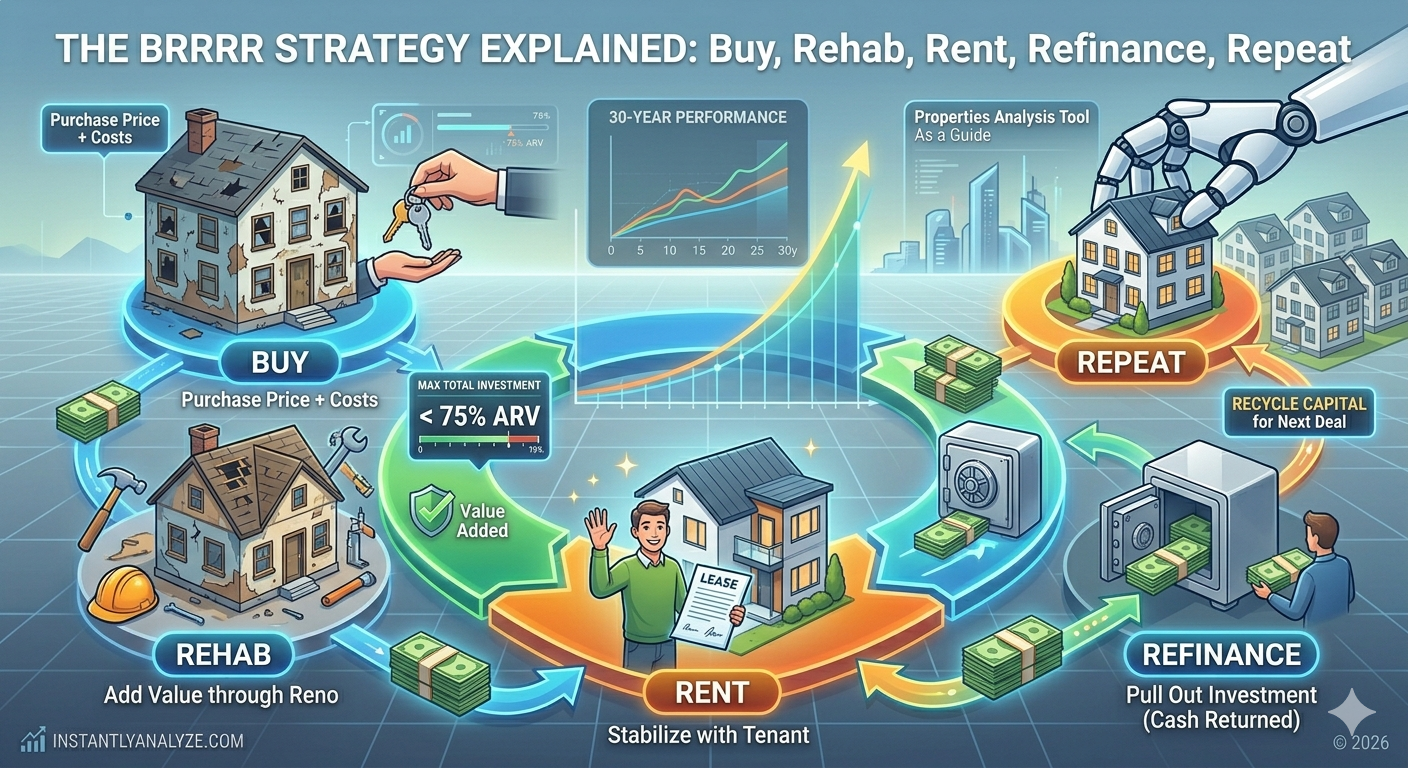

- BRRRR (Buy, Rehab, Rent, Refinance, Repeat) — forcing appreciation through renovation and recycling capital

- Short-term rentals — higher income potential but more active management

- REITs — passive exposure to real estate without owning property directly

The 1% rule applies specifically to traditional buy-and-hold rentals. It is not relevant for flips, REITs, or development deals.

What is the 1% rule in real estate

The 1 percent rule real estate investors use states that a rental property's monthly gross rent should be at least 1% of the all-in acquisition cost.

Formula:

Monthly Rent ÷ Total Acquisition Cost ≥ 1%

Total acquisition cost means purchase price plus any upfront repairs needed to make the property rentable. If you pay $180,000 for a house and spend $20,000 on repairs, your total is $200,000 and the 1% threshold is $2,000/month in rent.

Worked examples:

| Property Price | Upfront Repairs | All-In Cost | 1% Rent Target |

|---|---|---|---|

| $100,000 | $0 | $100,000 | $1,000/mo |

| $150,000 | $10,000 | $160,000 | $1,600/mo |

| $250,000 | $0 | $250,000 | $2,500/mo |

| $400,000 | $20,000 | $420,000 | $4,200/mo |

If a property rents at or above its target, it passes. If it falls short, move on unless there are unusual circumstances worth investigating.

How the 1% rule functions as a filter

The point of the rule is speed, not precision. When you're browsing 40 listings on a Sunday afternoon, you do not have time to build a full cash flow model for each one. The 1% rule lets you eliminate the obvious losers in 10 seconds per property and focus your energy on the handful worth deeper work.

It also gives you a market-comparison baseline. If you're evaluating deals in two different cities, the 1% rule creates a standardized ratio that makes them directly comparable regardless of price.

Applying the 1% rule: a practical walkthrough

Start with the asking price, add any upfront repairs needed before the property is rentable (zero for turnkey deals), and that sum is your all-in cost. Then find current market rent — check Zillow, Rentometer, or Craigslist for comparable rentals in the same neighborhood. Divide rent by all-in cost. If the result is 0.01 or higher, the property passes and goes on your short list. If it falls short, move on unless something specific makes it worth a second look.

Identifying properties that meet the 1% criteria

Properties are most likely to pass the 1% screen in:

- Lower-cost markets in the Midwest and Southeast where median home prices are under $200,000

- B and C class neighborhoods where the rent-to-price ratio is naturally higher

- Value-add deals where you can force appreciation and increase rents after renovation

Properties rarely pass in high-cost coastal markets where median prices exceed $500,000. In San Francisco or Seattle, the math almost never works. That does not mean coastal markets are bad investments — appreciation can still produce strong IRR — but the 1% rule is not the right filter there.

Free to use. No credit card needed. See cash flow, cap rate, and ROI in minutes.

Start Analyzing — FreeThe 2% rule in real estate: when stricter is better

The 2% rule real estate investors use applies the same formula at a higher threshold. Monthly rent should equal at least 2% of the all-in purchase price.

A $100,000 property needs $2,000/month to pass the 2% rule. That is a much higher bar than the 1% threshold of $1,000/month.

Key differences between the 1% and 2% rules

| 1% Rule | 2% Rule | |

|---|---|---|

| Monthly rent target | 1% of purchase price | 2% of purchase price |

| Markets where achievable | Midwest, Southeast, rural areas | Very low-cost markets only |

| Investor type | Most buy-and-hold investors | Cash-flow-maximizing investors |

| Difficulty in practice | Achievable with effort | Rare outside sub-$100K properties |

When to use the 2% rule

The 2% rule is most relevant when you are specifically hunting for maximum cash flow in markets where properties sell below $120,000. In Detroit, Cleveland, Memphis, and similar markets, the math can work. In most other U.S. markets, applying a 2% screen eliminates nearly every property on the market.

Some investors use the 2% rule specifically for the BRRRR strategy, where the goal is to pull out most of their capital at refinance and generate strong ongoing cash flow on minimal equity. If you need that level of return to make the numbers work after a refi, 2% is a reasonable screen.

For most investors in most markets, the 1% rule is the right threshold. The 2% rule is a specialized filter, not a universal standard.

Real estate investment tips: what matters beyond the 1% screen

The 1% rule tells you if a deal is worth a second look. It does not tell you whether the deal is actually good. Here is what to evaluate once a property passes the initial screen.

Operating expenses

The 1% rule only considers gross rent. It ignores everything that comes out of that rent before you see a dollar. A rough starting point is the 50% rule: expect operating expenses to consume about half of gross rent over time.

Operating expenses include:

- Property taxes

- Insurance

- Maintenance and repairs

- Vacancy (typically 5–10% of gross rent)

- Property management (8–12% if you use a manager)

- Capital expenditures (roof, HVAC, appliances)

A property at exactly 1% after a full expense load may generate very little cash flow. Run the numbers before assuming it is a good deal.

Location and market trends

Two properties can have identical rent-to-price ratios and produce very different outcomes if one is in a strengthening market and the other is in a declining one. Before committing, check:

- Population and employment trends in the metro area

- Vacancy rates for comparable rentals

- Recent rent growth (or stagnation)

- Neighborhood trajectory — improving, stable, or declining

Real estate investing advice that holds across all markets: location affects both your rental demand and your eventual exit price. A slightly lower-yielding property in a strong market often outperforms a higher-yielding one in a weak market over a 10-year hold.

The metrics that follow the 1% screen

After a property passes the initial filter, run these metrics before making an offer:

| Metric | What it tells you |

|---|---|

| Cap rate | Unlevered income return; good for comparing properties and valuing them against market norms |

| Cash-on-cash return | Annual cash yield on your actual cash invested; accounts for your financing |

| 50% rule | Quick expense estimate to project net operating income without itemizing every cost |

| IRR | Total annualized return over the full hold, including appreciation and exit proceeds |

Use the 1% rule to create a short list. Use these metrics to rank that list and make the final call.

A repeatable process for how to invest in real estate

Most experienced investors use the same sequence: screen with the 1% rule to create a short list, apply the 50% rule to estimate cash flow potential, calculate cap rate to compare the unlevered yield against market norms, then run cash-on-cash return to factor in your actual financing. If the numbers still hold up, run a full analysis before making the offer.

Our Properties Analysis Tool runs steps 3–5 automatically once you enter the purchase details and assumptions.

When the 1% rule fails

The rule is a shortcut, and shortcuts have failure modes.

In rising markets, property prices climb faster than rents and fewer deals pass the 1% screen — even though they may be sound investments on appreciation and IRR grounds. Do not reject an entire market because the 1% test fails.

The rule also has no expense awareness. A property in a high-tax state with an aging roof might clear the 1% threshold and still produce negative cash flow once real expenses are counted. Similarly, it says nothing about property condition, deferred maintenance, or flood zone risk.

Finally, the right threshold varies by market. Many experienced investors in coastal markets accept 0.6%–0.8% because appreciation makes up the gap. The 1% rule is a useful default, not a law.

Conclusion

The 1% rule is one of the most useful filters in real estate investing — not because it identifies great deals, but because it quickly eliminates bad ones. A core skill in how to make smart real estate investment decisions is evaluating more deals faster, and the 1% rule is where that process starts. In a market where you might look at dozens of properties before finding one worth pursuing, that elimination speed has real value.

Apply it as the first step, not the last. Once a property clears the screen, use cap rate, cash-on-cash return, and a full expense analysis to determine whether it actually makes sense to buy.

Ready to go beyond the 1% rule? Our Properties Analysis Tool calculates cap rate, cash-on-cash return, and IRR for any rental — give it a try before your next offer.

Also worth reading: cash-on-cash return, cap rates, and the 50% rule.