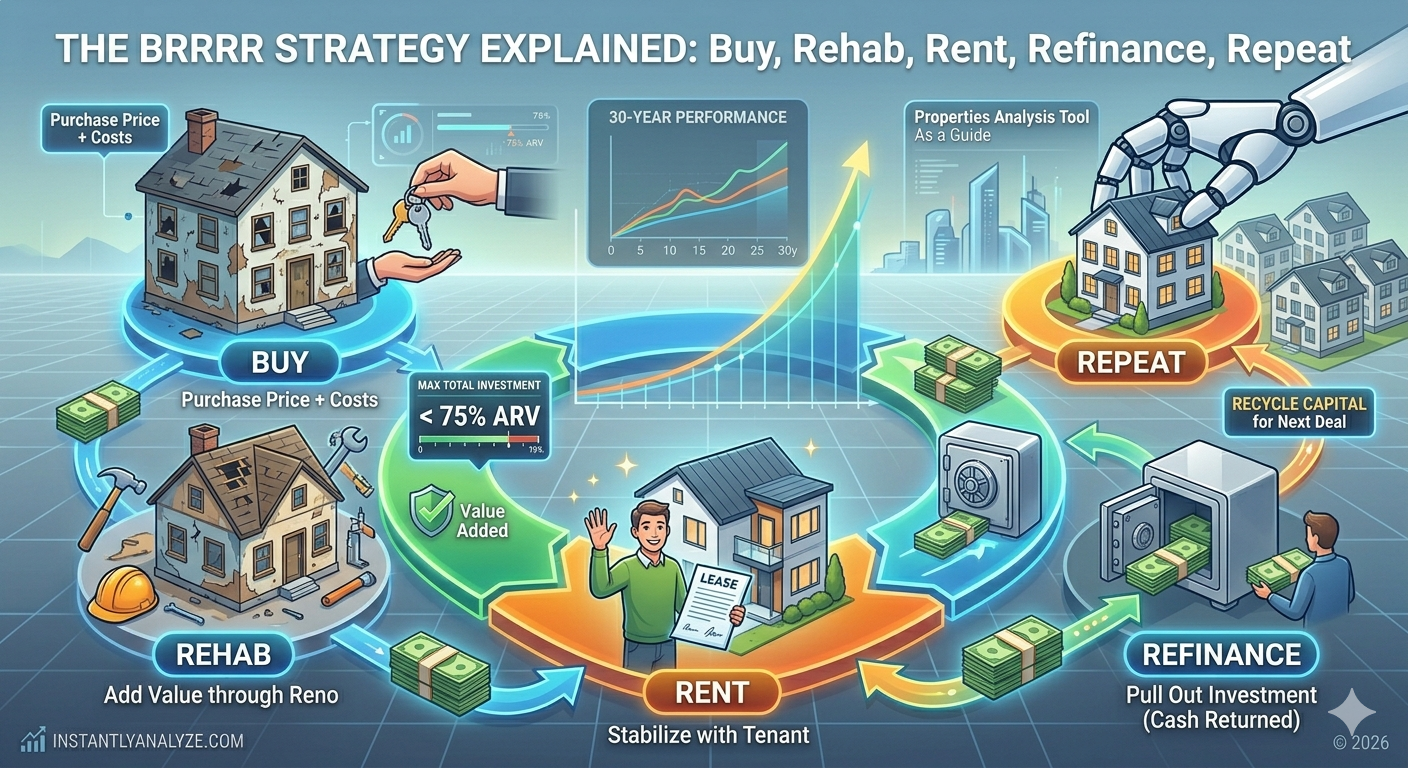

The BRRRR strategy is one of the most powerful methods for building a rental portfolio rapidly without tying up all your capital in each deal. When executed correctly, you can recycle the same pool of money across multiple properties — effectively buying rentals with little or no money left in the deal.

BRRRR stands for: Buy → Rehab → Rent → Refinance → Repeat

How BRRRR Works

The core idea: buy a distressed property at a discount, add value through renovation, rent it out to stabilize income, then do a cash-out refinance based on the improved value — pulling out most or all of your original investment.

The BRRRR Cycle

1. Buy: Purchase below After Repair Value (ARV)

2. Rehab: Renovate to increase value and appeal

3. Rent: Stabilize with a tenant at market rent

4. Refinance: Cash-out refi based on new appraised value

5. Repeat: Use pulled-out cash to buy the next property

Key Numbers: The BRRRR Spreadsheet

What is ARV?

After Repair Value (ARV) is the estimated market value of the property after renovations are complete. It's the foundation of every BRRRR calculation.

ARV = Comparable sales price per sq ft × Your property sq ft

Example: If renovated 3/2 homes in the neighborhood sell for $150/sqft and your property is 1,400 sqft:

ARV = $150 × 1,400 = $210,000

The 75% Rule

For BRRRR to work, your total investment must stay at or below 75% of ARV — leaving room for the lender to refinance and for you to pull your money out.

Max Total Investment = ARV × 75%

Max Total Investment = $210,000 × 75% = $157,500

So with a $210,000 ARV, your purchase price + rehab costs + holding costs must stay under $157,500.

Full BRRRR Example

| Item | Amount |

|---|---|

| Purchase price | $100,000 |

| Rehab costs | $40,000 |

| Holding costs (insurance, taxes, utilities during rehab) | $3,000 |

| Closing costs (purchase) | $2,500 |

| Total cash invested | $145,500 |

| ARV after rehab | $210,000 |

| Cash-out refinance (75% of ARV) | $157,500 |

| Cash returned to you | $157,500 − $145,500 = $12,000 left in |

In this example, you got most of your money back. The goal is to get to zero or negative (cash back in pocket) while still having a property that cash flows.

After the Refinance

Now calculate whether the property cash flows on the new loan:

- New mortgage: $157,500 at 7.5%, 30 years → ~$1,101/month

- Market rent: $1,600/month

- Operating expenses (45%): $720/month

- Monthly cash flow: $1,600 − $720 − $1,101 = −$221/month ← This is a problem

If the refi payment kills cash flow, the BRRRR doesn't work. This is the most common mistake.

Fix: You need either higher rent, lower expenses, or to keep more equity in the deal (borrow less).

When BRRRR Works Best

- Markets with value-add inventory: Distressed properties available below market

- Strong rental demand: Low vacancy, rising rents

- Favorable lending environment: Access to cash-out refi products

- Contractor relationships: Reliable crews at predictable costs

- Conservative ARV estimates: Err on the side of caution

Free to use. No credit card needed. See cash flow, cap rate, and ROI in minutes.

Start Analyzing — FreeBRRRR Risks to Manage

Rehab Cost Overruns

The #1 BRRRR killer. Always get 3 contractor bids, add a 15–20% contingency buffer, and never start until you have a signed contract with fixed-price items.

ARV Misjudgment

If comps don't support your ARV, the refi won't cover your costs. Run comps with a local agent before buying.

Seasoning Requirements

Most conventional lenders require 6–12 months of ownership before a cash-out refi. Plan your timeline accordingly.

Rental Market Weakness

If you can't get market rent after renovating, your cash flow suffers and the BRRRR math breaks down.

BRRRR vs. Traditional Rental Purchase

| Factor | Traditional Buy-and-Hold | BRRRR |

|---|---|---|

| Capital required | Full down payment stays in deal | Recycled (pulled back out) |

| Property condition | Move-in ready | Distressed/value-add |

| Timeline | Faster | 3–6 months longer |

| Skill required | Lower | Higher (rehab experience needed) |

| Scalability | Limited by capital | Faster portfolio growth |

Analyzing Your BRRRR Deal

Use our Properties Analysis Tool to:

- Model cash flow before and after the refinance

- Calculate cap rate and cash-on-cash return on the refi scenario

- Run the IRR over your full hold period

- See the deal verdict before you commit

Conclusion

BRRRR is a powerful strategy but requires more skill, patience, and capital management than a typical buy-and-hold. The investors who do it best are conservative on ARV, thorough on rehab bids, and realistic about cash flow after refinancing.

When all five steps execute correctly, you build a portfolio faster than traditional methods — with each deal recycling capital for the next one.

Modeling a BRRRR deal? Use our free property analysis tool to run the numbers on your buy, rehab, rent, and refinance scenarios.