Return on Investment (ROI) for rental properties is more nuanced than for stocks or savings accounts — because real estate generates returns through multiple channels simultaneously. This guide explains the right way to measure ROI, why simple ROI understates your actual returns, and which metric to use for different decisions.

Why Simple ROI Undersells Real Estate

The basic ROI formula:

Simple ROI = Annual Profit ÷ Total Investment × 100

For real estate, this only captures cash flow — missing three other major return drivers:

- Appreciation: Property value increases over time

- Loan paydown: Your tenant's rent pays down your mortgage principal

- Tax benefits: Depreciation, mortgage interest deduction, and other shelters

A property that barely breaks even on cash flow might still deliver 15%+ total annual returns when you factor all four.

The Four Sources of Real Estate ROI

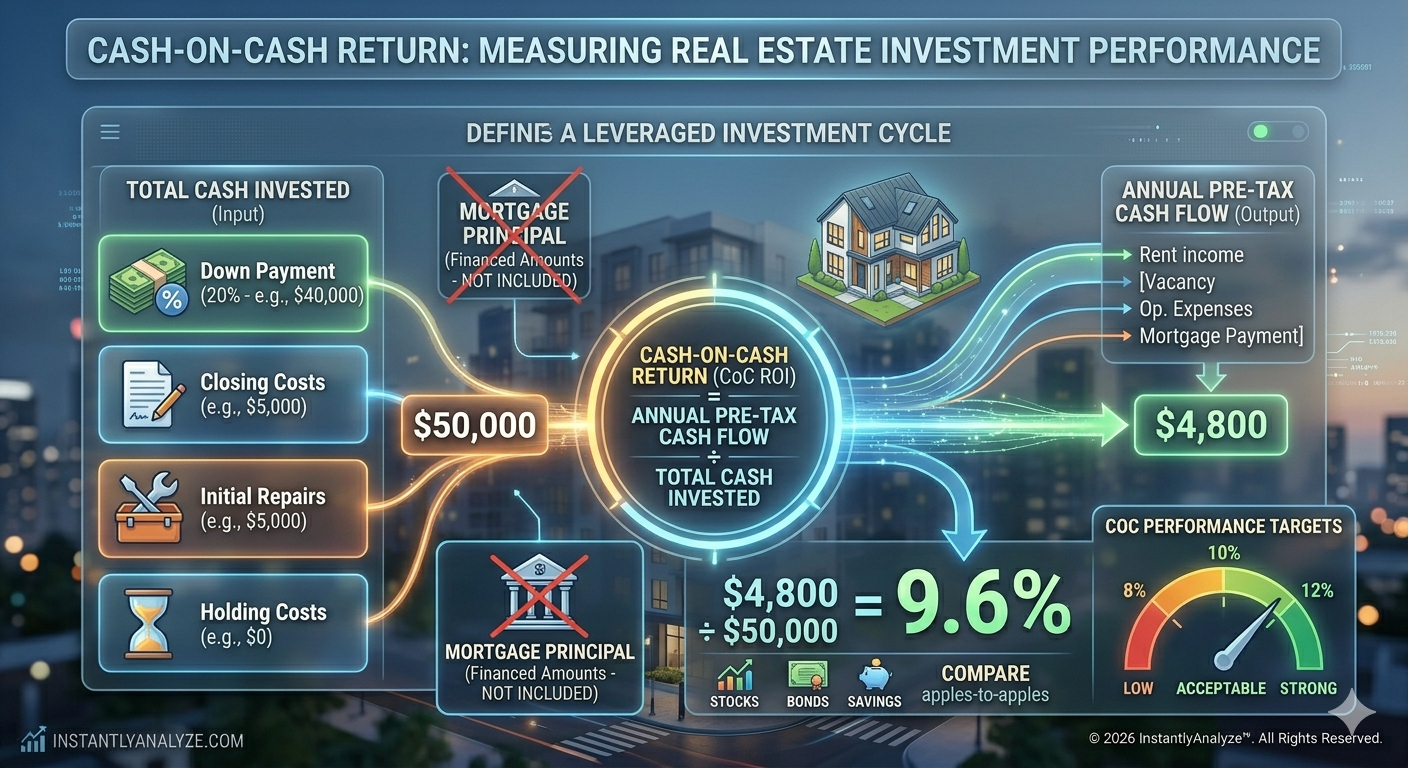

1. Cash Flow Return

The monthly net income after all expenses and mortgage payment.

Annual Cash Flow = (Gross Rent − Expenses − Mortgage) × 12

Cash Flow ROI = Annual Cash Flow ÷ Total Cash Invested

Example:

- Monthly cash flow: $200

- Cash invested: $55,000

- Cash flow ROI: ($200 × 12) ÷ $55,000 = 4.4%

This is also called Cash-on-Cash Return (CoC ROI). See our full guide on CoC ROI.

2. Appreciation Return

Real estate appreciates at roughly 3–5% nationally, though markets vary widely.

Appreciation Return = (Annual Appreciation ÷ Cash Invested) × 100

Example:

- Property value: $250,000

- Annual appreciation (3%): $7,500

- Cash invested: $55,000

- Appreciation ROI: $7,500 ÷ $55,000 = 13.6%

Note: This leveraged return is why real estate ROI can be so high. A 3% appreciation on a $250,000 property is a 13.6% return on your $55,000 cash investment.

3. Loan Paydown Return

Every mortgage payment reduces your principal balance — building equity.

Example (Year 1 of 30-year, $200K at 7% loan):

- Total payments: $15,966

- Interest paid: $13,953

- Principal paid (equity built): $2,013

- Loan Paydown ROI: $2,013 ÷ $55,000 = 3.7%

This increases each year as the interest portion shrinks.

4. Tax Benefits

Depreciation allows you to deduct 1/27.5 of a residential property's value each year from your taxable income.

Example:

- Building value (excluding land): $200,000

- Annual depreciation deduction: $200,000 ÷ 27.5 = $7,273

- At a 25% tax rate, this saves: $1,818/year

- Tax benefit ROI: $1,818 ÷ $55,000 = 3.3%

Total ROI: Adding It All Together

| Return Component | Annual Amount | ROI % |

|---|---|---|

| Cash flow | $2,400 | 4.4% |

| Appreciation | $7,500 | 13.6% |

| Loan paydown | $2,013 | 3.7% |

| Tax benefits | $1,818 | 3.3% |

| Total Annual Return | $13,731 | 25.0% |

A property that appears to yield 4.4% in cash flow actually delivers 25% total return — that's the power of leveraged real estate investing.

Free to use. No credit card needed. See cash flow, cap rate, and ROI in minutes.

Start Analyzing — FreeWhich ROI Metric to Use When

| Decision | Best Metric |

|---|---|

| "Does this pay me monthly?" | Cash-on-Cash Return |

| "Is this property fairly priced?" | Cap Rate |

| "How does this compare to stock investing?" | Total ROI or IRR |

| "Should I sell now or hold?" | IRR with projected exit |

| "How quickly do I get my money back?" | Equity Multiple |

Benchmarks: What's a Good ROI?

| Metric | Minimum | Target | Excellent |

|---|---|---|---|

| Cash-on-Cash | 5% | 8%+ | 12%+ |

| Cap Rate | Market rate | Market + 1% | Market + 2% |

| Total ROI | 10% | 15–20% | 20%+ |

| IRR (10-year) | 10% | 13–16% | 18%+ |

The ROI Calculation Pitfalls

Forgetting closing costs

Your cash invested includes the down payment plus closing costs ($4,000–$8,000 on a typical purchase). Leaving these out inflates your ROI.

Ignoring management time

If you self-manage, you're contributing labor. At minimum, model 10% management fees to get an honest picture.

Using proforma numbers

Always use actual current rents and verified expenses — not the seller's projections.

Underestimating CapEx

Major repairs and replacements reduce your effective cash flow and ROI significantly over a long hold.

Calculate Your Rental Property ROI

Our Properties Analysis Tool calculates all four return components automatically:

- Cash flow and CoC ROI month-by-month

- Cap rate vs. market

- 30-year projection with appreciation and loan paydown

- IRR over your target hold period

Get your complete ROI picture in under 2 minutes — no spreadsheet needed.

Understanding ROI is critical. Explore our guides on cash-on-cash return, cap rate, and IRR to master every metric.